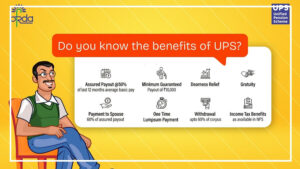

National Pension System (NPS) subscribers can withdraw their full retirement savings — but only under certain conditions.

The amount you can take out depends mainly on your total corpus at retirement and when you choose to exit.

Recently, the withdrawal rules were updated to give small investors more flexibility.

Here’s how the new system works.

When Can You Withdraw 100% of Your NPS Corpus?

If you retire at age 60 or later and your total NPS corpus is up to Rs 8 lakh, you can withdraw the entire amount as a lump sum.

Earlier, this limit was Rs 5 lakh.

It has now been increased to Rs 8 lakh, offering more relief to small-corpus subscribers.

If your total savings fall within this limit, you do not need to buy an annuity.

You can take the full amount at once.

What If Your Corpus Is Higher?

The rules change if your retirement savings are above Rs 8 lakh.

Here’s how it works:

If your corpus is between Rs 8 lakh and Rs 12 lakh:

You can withdraw up to Rs 6 lakh as a lump sum.

The remaining amount must be withdrawn gradually or used to buy an annuity.

If your corpus is above Rs 12 lakh:

You can withdraw up to 80% as a lump sum.

At least 20% must be used to purchase an annuity.

An annuity ensures that you receive a regular pension income after retirement.

These changes aim to balance immediate cash needs with long-term financial security.

Other Key Changes You Should Know

The Pension Fund Regulatory and Development Authority (PFRDA) introduced these reforms to make NPS more flexible and investor-friendly.

One important update is that subscribers can now remain invested in NPS until the age of 85.

Earlier, the limit was lower.

There is also a provision for partial withdrawals during the account’s tenure.

Subscribers can withdraw up to 25% of their own contributions for specific needs, such as:

Medical emergencies

Higher education

Marriage

Buying or building a house

However, certain conditions apply.

What Do These Changes Mean for You?

The updated withdrawal framework gives retirees more liquidity, especially those with smaller savings.

At the same time, it ensures that larger corpus holders still have a steady pension income through mandatory annuity investment.

In simple terms, NPS continues to function as a long-term retirement tool — but with more flexibility than before.

If you are planning your retirement, understanding these rules can help you make smarter decisions about when and how to exit your NPS account.